The challenges with most car allowances

An auto allowance has three drawbacks:

1. Tax Waste

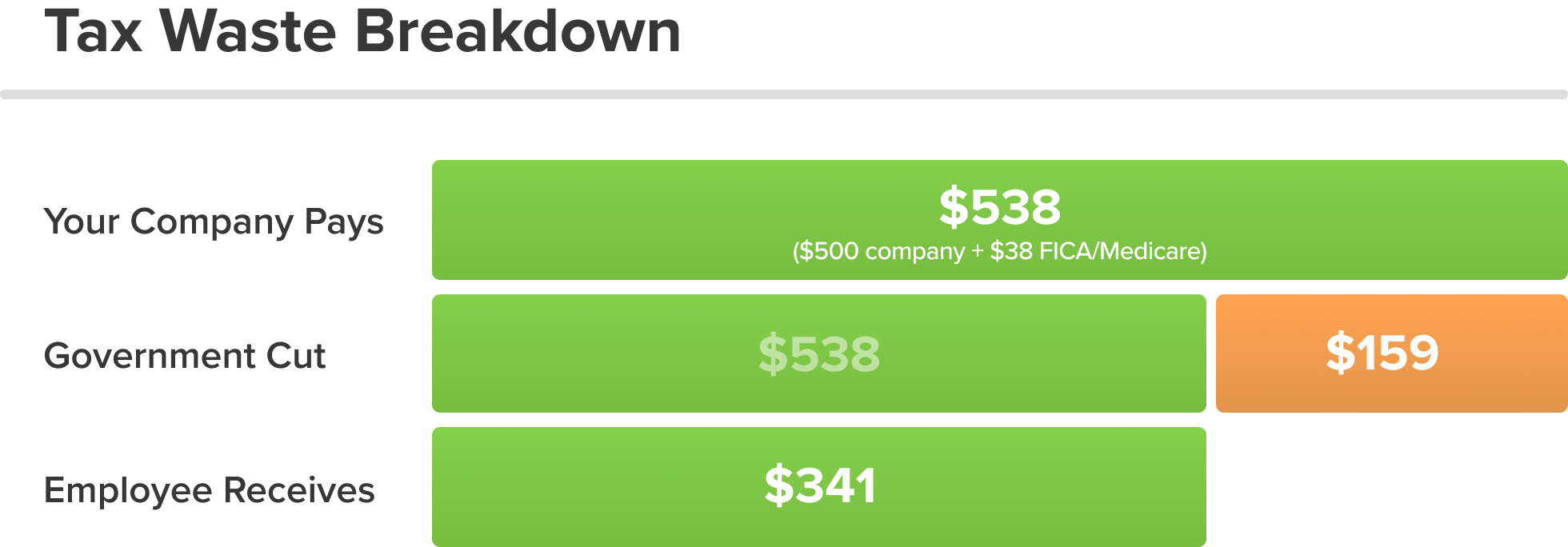

Given a $600 monthly allowance, how much actually goes to pay vehicle expenses? Less than you’d think. An employee in the 24% tax bracket will take home only $410.10 after subtracting both income taxes and FICA/Medicare. That amount will decrease further if the car is garaged in a state that levies an income tax.

On top of this, the company pays $45.90 for FICA/Medicare on that $600. Here's an infographic representing the same calculations applied to a $500/month allowance:

Given the vehicle expenses an allowance should cover – gas, maintenance, depreciation, insurance, etc. – will that $341 truly suffice? or the $410, if you pay a $600 allowance? Because the IRS considers a car allowance a taxable benefit and not an expense reimbursement, employees are left playing catch up. Why not divert the tax money away from the government and back into your organization?

How much can you save?

2. Variations in expenses

A single employee’s expenses can vary month to month. Two different employees in the same company can have widely different expenses. Gas prices rise and fall, territory sizes differ, and geographically sensitive expenses can vary widely.

Compare the average fuel and insurance costs between three different states from 2025 (expenses have increased significantly since then):

Paying everyone the same amount can create fairness problems, shortchange some employees, and lead to undesirable employee behavior, such as curtailing business trips to save money.

3. Lack of precision

As recently as 2022, mBurse's Annual Auto Allowance Survey revealed that only a quarter of companies calculated their car allowance using vehicle expense data. And 73% had gone ten years or more since last updating the allowance amount.

In next year's survey, 62% reported employee complaints about the car allowance. How can anyone expect their allowance to meet all employees’ needs when the amount is based on no data and goes unreviewed for years?

How to boost car allowance take-home amounts

Bad options:

- Boost everyone's car allowance company-wide (taxes!)

- Switch to a mileage rate or add a fuel card (too expensive)

- "Just write it off on next year's taxes" (not possible indefinitely)

Taxes eat up 30-40% of a typical allowance. Mileage rates incentivize over-reporting of mileage (or unnecessary driving). Fuel cards are not cost-effective. Employees cannot deduct unreimbursed business expenses, including business mileage. (Only independent contractors can.)

Solutions to the Big Three challenges of car allowances:

As you can see, taking any step to address the shortcomings of car allowances will cost time or money or both. Most solutions require adding a mileage log as well. But to do nothing will cost more in the long run.

Car

Allowance

Best Practices

Simply switching to a mileage reimbursement like the IRS mileage rate cannot solve the problems of expense variations and lack of precision and adds a new challenge: cost control. (See Why the IRS Rate Overpays Some Workers and Underpays Others.)

Only a fixed and variable rate car allowance can eliminate tax waste while solving these problems. We’ll explain this, and how a FAVR program is more cost-effective. But first, let’s look at how your car allowance policy impacts every aspect of the company.

How your car allowance affects your company

Getting the vehicle policy right or wrong can impact numerous parts of an organization.

We’ve already covered tax waste and inequitable compensation of employees due to expense variations. But there’s also a domino effect that touches other aspects of an organization:

Risk management for employee drivers

If you fail to sufficiently reimburse all employees, you open the door to labor code lawsuits and to employees taking risky measures to cut costs. For example, an employee might reduce insurance coverage.

If that employee causes a car accident while working, your company’s insurance may be forced to close the gap between the employee’s insurance and the costs of the accident.

Is your

company exposed?

Mobile workforce productivity

Under-reimbursed employees may also recoup lost income by reducing the amount of driving they do. Reduced travel can mean fewer face-to-face meetings with clients and potential clients. Over time, less driving may compromise sales productivity and client relations.

Attraction and retention of employees

Some employees will leave if they cannot obtain equitable reimbursement. Check your attrition rates. If you have not adjusted the allowance or reimbursement recently, don’t be surprised if attrition has increased. Similarly, if prospective employees project insufficient reimbursement, they may not seek or accept a job at your company.

How to calculate the right car

allowance for 2026

Rising taxes, inflation, and higher fuel costs are putting new pressure on organizations across the U.S. These conditions make it more urgent than ever to implement a fair, modern vehicle reimbursement policy for 2026.

We are in the sixth year of a tax policy that prevents employees from writing off business mileage and other unreimbursed expenses. In an inflationary economy, workers face significant financial anxiety.

Companies that adjust to these realities have a competitive advantage over those that don't.

Now is the time to take concrete steps to investigate and adjust your company's car allowance policy:

In the wake of the lost tax deduction that took effect in 2019 and the inflation that occurred from 2021 to 2026, mobile employees are seeking recourse. While some may drive less or look for new employment, others may take legal action under state labor laws, including class-action lawsuits.

1. Estimate actual employee vehicle expenses and compare these with your current allowance amount. Then calculate the car allowance amount needed to close any gaps.

2. If you’re paying a taxable car allowance, calculate how much your organization could save by switching to a tax-free plan. The elimination of tax waste could fully close the gaps.

3. If you’re using a fuel card or reimbursement, calculate whether fuel consumption matches business productivity and whether your organization is properly limiting personal use.

4. Learn more about the fixed and variable rate car allowance. FAVR is the most accurate and legally defensible policy type, and it's inflation-proof and tax code-compliant because it ensures accurate reimbursement.

How much is a fair

car allowance?

The question remains: How much car allowance should you pay in 2026?

Hopefully, you’ve figured out the answer: It’s complicated!

Because mobile employees within the same organization can experience widely different costs, there’s no quick and easy way to determine the right amount. Without knowing an employee’s mileage and zip code and the size of vehicle required to carry out the job, it’s impossible for someone to tell you the right amount.

But there are some clear-cut principles that you can follow:

1. One-size-fits-all CANNOT be your solution.

Because car expenses among employees vary, the car allowance should vary. A small company with a narrow range of employee expenses may get away with a standard allowance amount, but even then there will be disparities between expenses and reimbursement for some employees – and tax waste will remain a problem.

2. Territory size MUST factor into the car allowance calculation.

Mileage affects everything from fuel consumption and tire wear to maintenance and depreciation. Employees with larger territories drive more, and should be reimbursed more. Failing to incorporate mileage into the amount will result in low productivity from shortchanged employees.

3. Geographically-based costs MUST affect the car allowance calculation.

The costs of gas, insurance, taxes, registration/license, and maintenance are regionally sensitive. It’s vital to calculate, given a reasonably-sized vehicle in a particular zip code, what each employee’s expenses should be. Incorporate that data into the allowance calculation.

With nationwide fuel price increases, it is paramount that the costs be updated monthly to keep pace with employees' out-of-pocket expenses.

Data needed to calculate a fair car allowance

Different employees should receive different amounts and those amounts should be based on actual data. This is the only way to ensure equitable reimbursement and to prevent over-reimbursing and under-reimbursing.

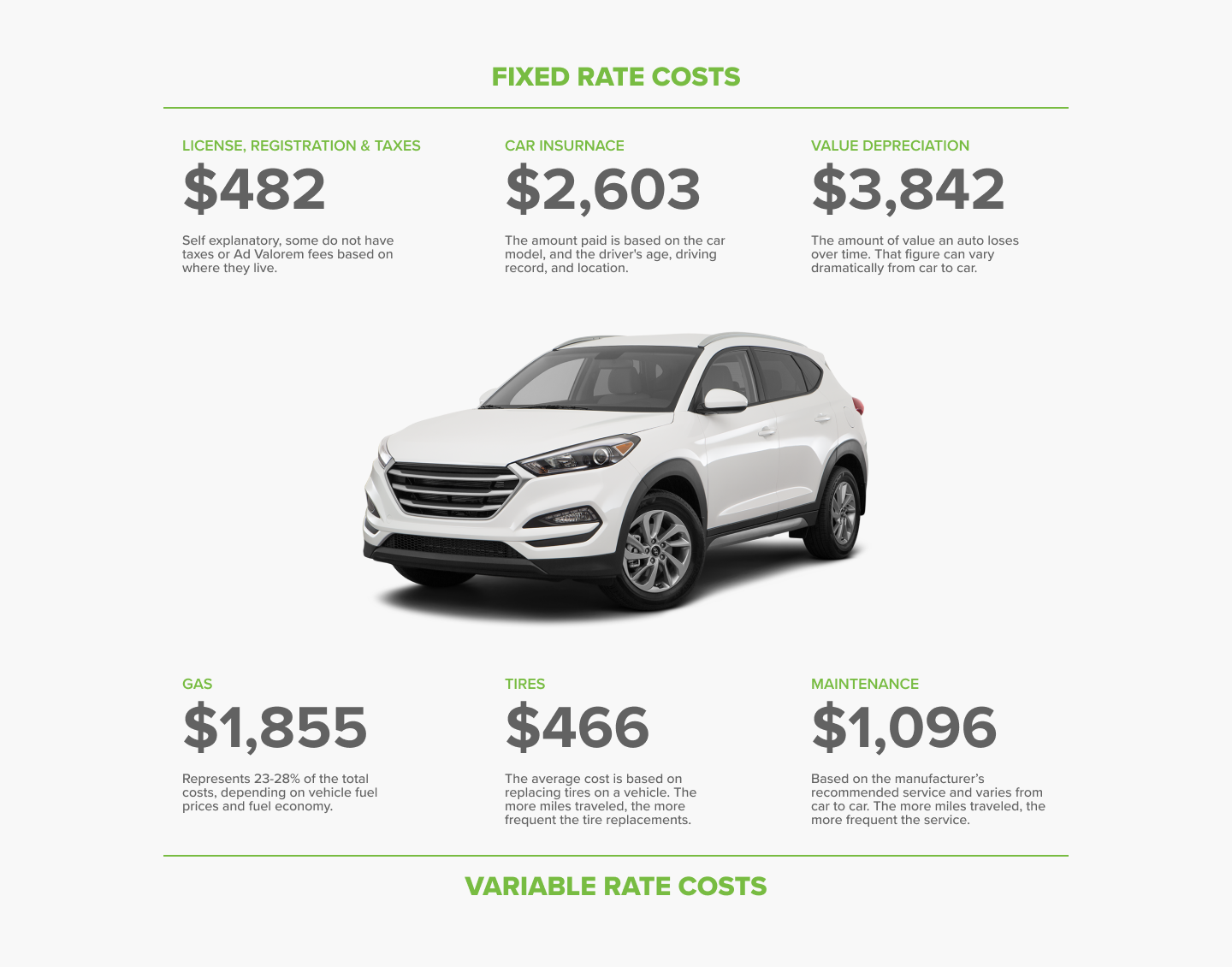

To get started, use the graphic below to discover the average costs of owning and operating a vehicle by expense category. You might be surprised at what you find.

These average annual costs amount to a monthly expense of $615.50. And that’s average. Will a $600/month taxable car allowance cover the costs of the average American driver? No way! After taxes, that $600 might be as little as $400.

What about a driver in California, where gas and maintenance prices are through the roof? Or in Michigan, where insurance rates are the highest in the country?

Those drivers' monthly vehicle expenses could easily reach $1,000.

Would a mileage reimbursement work better? Not necessarily. Depreciation and insurance together make up 60% of vehicle costs. That poses problems for low-mileage drivers since fixed costs are only marginally affected by miles driven.

What's your optimal car allowance for 2026?

You could use these average costs to estimate individual employees' needs, based on whether they face below-average or above-average costs, depending on location, territory size, and vehicle type. But more specific data exists.

To obtain data specific to select vehicle types and a selection of geographic locations, see our additional guide to the process of pinpointing that optimal allowance or reimbursement rate: Four Steps to a Reasonable 2026 Car Allowance.

Or you can complete our three-step process below to audit your current car allowance, conduct a competitive benchmarking analysis, and receive a free, optimized rate.

Even simpler, contact mBurse to find out about the vehicle allowance program administration. You don't administer your own health insurance, so why administer your own car allowance?

Find out how much a fair car allowance is this year.

Partner with experts who make saving your company and people money easy.